Does Investor Choice Actually Matter for Startup Success?

Does Investor Choice Actually Matter for Startup Success?

Synthesizing Insights From the Data

👋 Hi, I’m Andre and welcome to my weekly newsletter, Data-driven VC. Every Tuesday, I publish “Insights” to digest the most relevant startup research & reports, and every Thursday, I publish “Essays” that cover hands-on insights about data-driven innovation & AI in VC. Follow along to understand how startup investing becomes more data-driven, why it matters, and what it means for you.

Brought to you by Tegus - Quality Content Led by Top Investment Firms

Did you know that over 50% of VC firms on the prestigious Midas List conduct their expert calls through Tegus? This isn't just any transcript library; it's a goldmine of high-quality insights fueled by the world’s top investors.

Tegus is the only platform that allows you to delve into prominent VCs' minds and explore what they care most about when evaluating real investment opportunities.

Different Investors Have Different Philosophies. Find the One That Fits Your Needs

As entrepreneurs navigate the lifecycle of a startup from pre-seed to exit, the decision of which investor to partner with is more akin to a long-term marriage than a simple monetary transaction. This week, we aim to add a scientific foundation to the age-old debate about the actual value investors bring to the table—a discussion often mired in strong opinions and anecdotal evidence.

Different venture capital firms offer varying philosophies and strategies: From "kingmaker" firms like Tiger or Coatue, who deploy extensive amounts of capital to gradually dry out competitors, to more hands-on boutique firms like Benchmark or USV, who help with advise, facetime, and extensive networks.

We'll explore three key aspects of investor choice that can significantly impact a startup's path: the negotiation terms between VC and entrepreneur, the real impact of an investor's added value, and how to pick the right investor.

While we delve into how these factors can shape a startup's future, it's crucial to remember that the ultimate success of a business mostly rests on the founders - their vision, background, and execution - as we showed in our past few episodes on startup success and failure.

1) Investment Terms

A paper by Ewens et al. (2021) analyzes 8,100 first-round VC financings from 2002 to 2015, making it one of the largest datasets studied for such analysis to date. They were specifically interested in how negotiating terms between VCs and founders impact startup success.

Optimal Equity Share: The average startup’s value increases with the lead investor’s equity share up to an ownership stake (upon conversion) of 15%. Any further increase in the VC’s share decreases firm value.

2023 data from Carta shows median round dilutions of 20% for Seed & Series A, 17% for Series B, 13% for Series C, and 10% for Series D. It’s all about finding the right balance between investor equity stake to create sufficient buy-in and keeping founder dilution reasonable to keep them motivated, with sufficient skin in the game.

The above-mentioned study also analyses other contract terms which we combined with findings from Amore & Conti (2023) and Hong et al. (2020) to yield the following rundown of the most common deal terms and their impact on the startups:

VC Board Seats: These can diminish firm value by reducing entrepreneur control, though they may be very beneficial in deals with high-quality VCs.

Participation Rights: Often called “pro-rata” rights, they generally have a neutral effect on the likelihood of startup success while increasing the VC's share of the firm's value.

Pay-to-Play Provisions: Shift value towards the entrepreneur and can enhance firm value by penalizing VCs who don't reinvest in future rounds, thus facilitating the next fundraise. They can be somewhat of a double-edged sword though, as they might preclude top-tier funds from investing altogether.

✈️ KEY INSIGHTS: Founders should not sell more than 20% of their equity in the first priced round and be very careful which investors they onboard. VC board seats can make a big difference, but only if the board member has an exceedingly relevant background and/or network.

2) How Do Investors Add Value?

All papers examined so far state the importance of the quality of the VC and the entrepreneur as crucial in determining the terms negotiated, with both higher-quality VCs and founders typically able to secure more favourable terms.

Since we already know from our last episodes what makes a high-quality founder, we focus on what makes a good VC with a high potential for value add below. Many papers [1, 2, 3, 4] suggest that top tier VC firms can add value in every funding stage, with a slightly higher potential at the earlier stages. In the earlier stages, the value added is through network and domain expertise, and in the later stages through professionalisation and governance.

The influential study by Ewens et al. (2021) also found that the quality of the VC significantly impacts the success rate of startups. Experienced and well-connected VCs (top 10%) often negotiate terms that are favourable to them but also add substantial value to the startup, enhancing its chances of a successful exit through strategic guidance, network opportunities and the strong signalling effect of such investments (Conti et al., 2013).

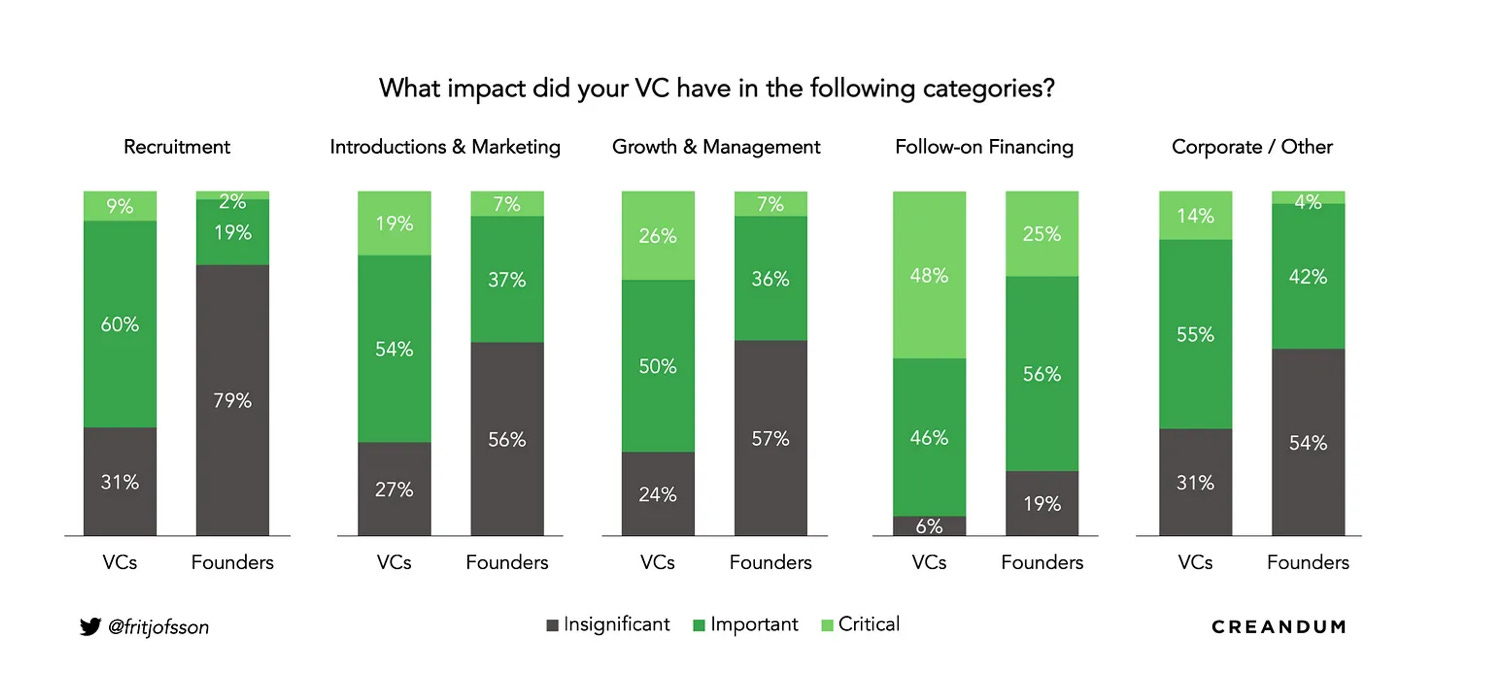

Chemmanour et al. (2011) found the reason in an increase in a startup’s efficiency, measured in total factor productivity after a venture capital injection (mostly through quicker and better automation). All these studies seem to converge on the fact that VCs can add substantial value but that this almost exclusively goes for the top funds. A 2022 survey by Creandum underlines this issue by pointing out that most funds overestimate the value that they bring to their portfolio companies.

Unsurprisingly, Croce et al. (2021) found that startups backed by angel investors with a strong track record in early-stage investments tend to attract follow-on venture capital funding much more effectively. This “herding effect” comes largely because experienced angels are considered quality signals to VCs (and same for early-stage VCs signalling to growth-stage VCs), indicating that the startup has solid foundations and growth potential. Additionally, startups that combine angel funding with VC support often secure more funding and have better chances of achieving successful exits, such as IPOs or acquisitions.

✈️ KEY INSIGHTS: Top-tier VCs add value through networking and expertise in the early stages and improve governance later on. Startups backed by experienced angel investors often attract more VC funding, increasing their chances of securing higher investments and achieving successful exits. The “herding effect” is real.

3) The Science (and Art) of Picking the Best Investors

Picking the right investor for your company can be one of the most difficult decisions you have to make. Especially in the current environment where you might find it even harder to get any financing at all.

If you are looking for an effective heuristic to judge potential investors, go by network and past performance. The “State of European Tech 2023” report by Atomico emphasizes the importance of well-networked VC firms, as they tend to experience better fund performance and successful exits.

Plummer et al. (2016) highlight the advantages of affiliations with investors that offer mentoring, access to resources, and ongoing performance monitoring. Startups should seek investors who provide substantial support beyond the capital, as this can significantly impact their growth and development.

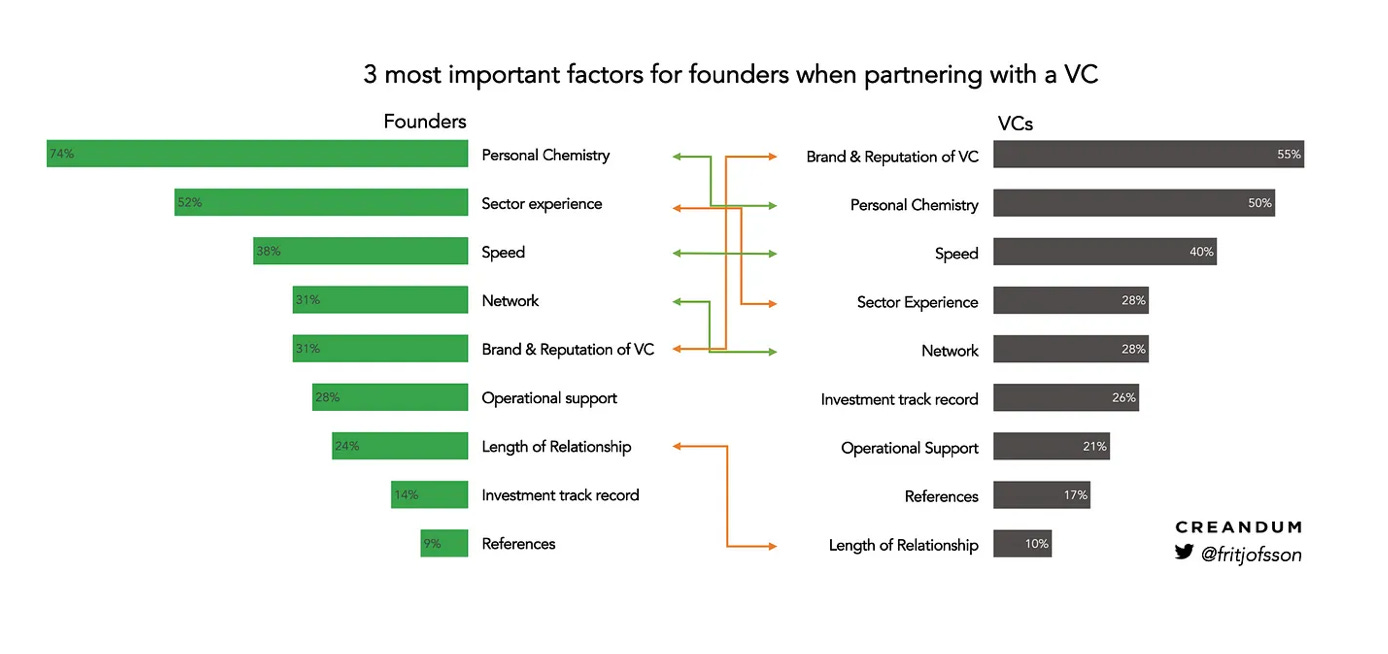

Lastly and maybe most importantly, be very honest about the personal chemistry you have with potential investors. The Creandum survey we mentioned above found that personal chemistry is the number one criterion most successful entrepreneurs look out for! If things go well, this is a looong journey.

✈️ KEY INSIGHTS: The best indicators that you are talking to a great investor are a) the quality of their network and b) past fund performance. However, none of this matters if the personal chemistry between you and an investor isn’t top-notch!

Conclusion

The scientific research on this week’s topic was not quite as uniform as it was for previous episodes, but there are key takeaways that strongly suggest that not all venture capital firms are created equal: from large assets aggregators with deep pockets (or “king makers”) to boutique firms with hands-on support (“handcraft”).

Studies highlight that keeping individual VC equity below 20% in initial rounds can optimize firm value and maintain founder motivation. Moreover, the top 10% of high-quality VCs add significant value, especially in the early stages through strategic guidance and robust networking, which are pivotal for successful exits.

In essence, the choice of investor is a critical and permanent one, impacting the startup's trajectory towards success. We don’t think this article will settle the debate anytime soon, but we hope it can contribute to providing a scientific basis to make a well-informed decision.

Thanks to Jérôme Jaggi for his help with this post.

Stay driven,

Andre

PS: Today is the 3rd day of the Data-Driven VC Summit 2024 and you can rewatch all sessions until Thursday night. It’s not too late to join us!

Thank you for reading this episode. If you enjoyed it, leave a like or comment, and share it with your friends. If you don’t like it, you can always update your preferences to receive just the regular Thursday “Essays”, just the Tuesday “Insights”, or both. Subscribe below and follow me on LinkedIn or Twitter to never miss data-driven VC updates again.

What do you think about my weekly Newsletter? Love it | It's great | Good | Okay-ish | Stop it

If you have any suggestions, want me to feature an article, research, your tech stack or list a job, hit me up! I would love to include it in my next edition😎