👋 Hi, I’m Andre and welcome to my newsletter Data-Driven VC which is all about becoming a better investor with Data & AI. Join 33,280 thought leaders from VCs like a16z, Accel, Index, Sequoia, and more to understand how startup investing becomes more data-driven, why it matters, and what it means for you.

Brought to you by Affinity – Navigating 2025’s Investment Landscape

Market consolidation is reshaping venture capital, with fewer firms capturing the lion’s share of deals. How can investors adapt their dealmaking strategies to stay ahead?

Join Mercedes Bent, Venture Partner at Lightspeed, and Brian Murphy, Lead Data Scientist at Salesforce Ventures on May 8 for key insights on evolving dealmaking trends, the behaviors of top-performing firms, and the strategies investors are using to thrive in a competitive market.

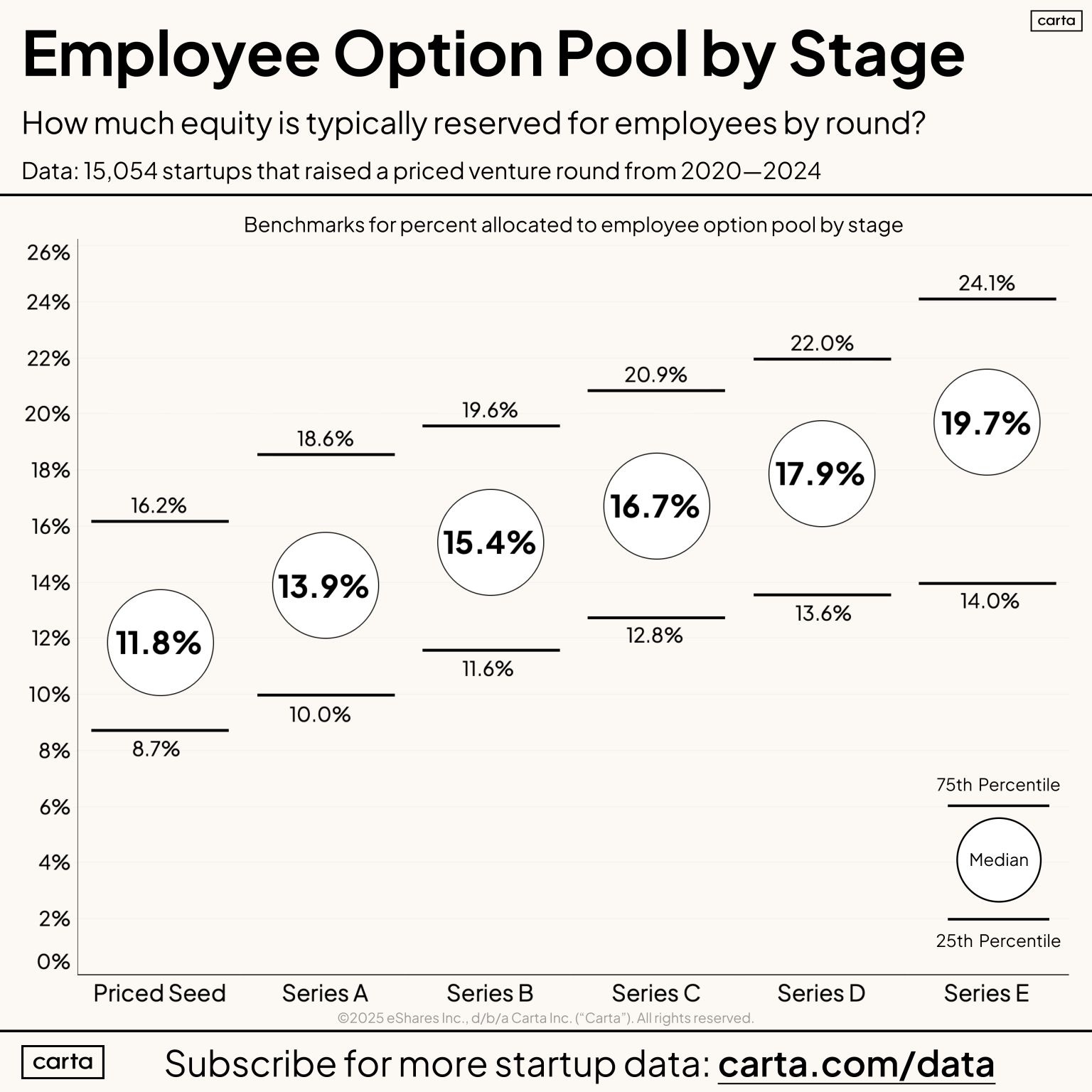

Sizing Options Pools per Stage

Most new investors require option pool increases pre round so that they dilute all existing shareholders. There’s an incentive for new investors to push for bigger increases as it reduces the likelihood and size of potential future increases (that they need to bear themselves once being a shareholder). Peter Walker from Carta analyzes data from over 15,000 startups and shares what option pool sizes look like by stage.

Median Seed-Stage Pool Size: The median post-round option pool size sits at 11.8%, based on analysis of startups that raised funding over the last five years.

Dilution Mechanics: Founders typically bear the brunt of pool expansions, especially when SAFEs convert at fundraising without participating in additional dilution.

Pool Utilization Rates: Most companies only use 60% to 70% of their employee pools before their next fundraising round, suggesting careful sizing is essential to avoid unnecessary dilution.

✈️ KEY TAKEAWAYS

It’s important to balance option pool increases so that they’re sufficient for short- and mid-term hiring, yet don’t overly dilute founders and investors too early. Take it step-by-step, look at the hires for the next 24 months, and have new investors take their part in the future too.

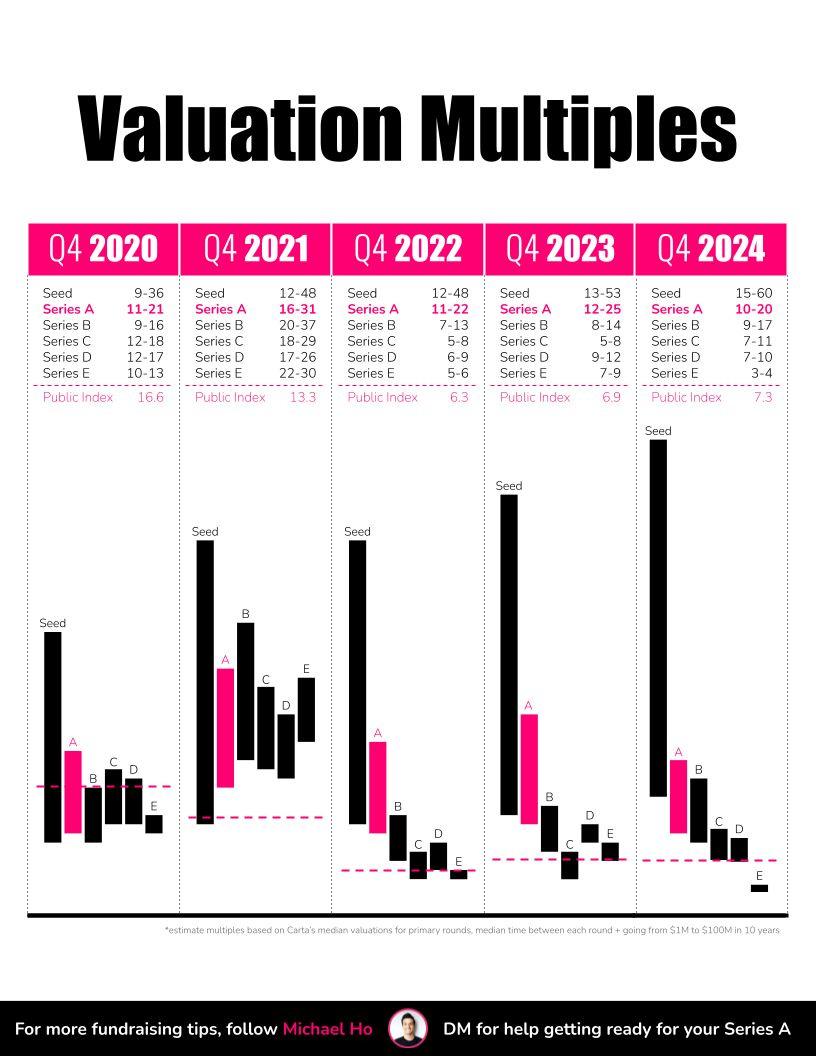

How Valuation Multiples Shifted from 2020 to 2024

Michael Ho dives into how startup valuation multiples have evolved over the past four years using Carta data. His modelling tracks how median pre-money valuations and growth assumptions map to changing venture expectations.

Seed Stage Multiples: Seed rounds in 2020 assumed startups would grow from $1M to $100M revenue in 10 years, but multiples have compressed significantly by 2024.

Time Between Rounds: The median time between rounds historically hovered around 18 months, though volatility has increased recently.

Public SaaS Comparison: The SaaS Capital Index shows that private startup multiples have moved closer to public SaaS valuations, particularly post-2022 corrections.

✈️ KEY TAKEAWAYS

Startup valuation expectations have become more conservative, aligning closer with public market realities and pressuring founders to show stronger, faster growth, specifically at the later stages.