👋 Hi, I’m Andre and welcome to my newsletter Data-Driven VC which is all about becoming a better investor with Data & AI. Join 31,600 thought leaders from VCs like a16z, Accel, Index, Sequoia, and more to understand how startup investing becomes more data-driven, why it matters, and what it means for you.

Brought to you by Deckmatch - Agentic Workflows and APIs for Data-Driven VCs

Connect your top-of-funnel to Deckmatch and transform pitch decks and URLs into structured and insightful data. Get detailed firmographic and people data, in-depth competitive and market analysis, and personalized investment memo without lifting a finger. The cherry on the cake? It's all seamlessly synced to your preferred tools like Affinity through our API integrations.

Never miss a deal, ditch the donkey work, and build meaningful relationships faster.

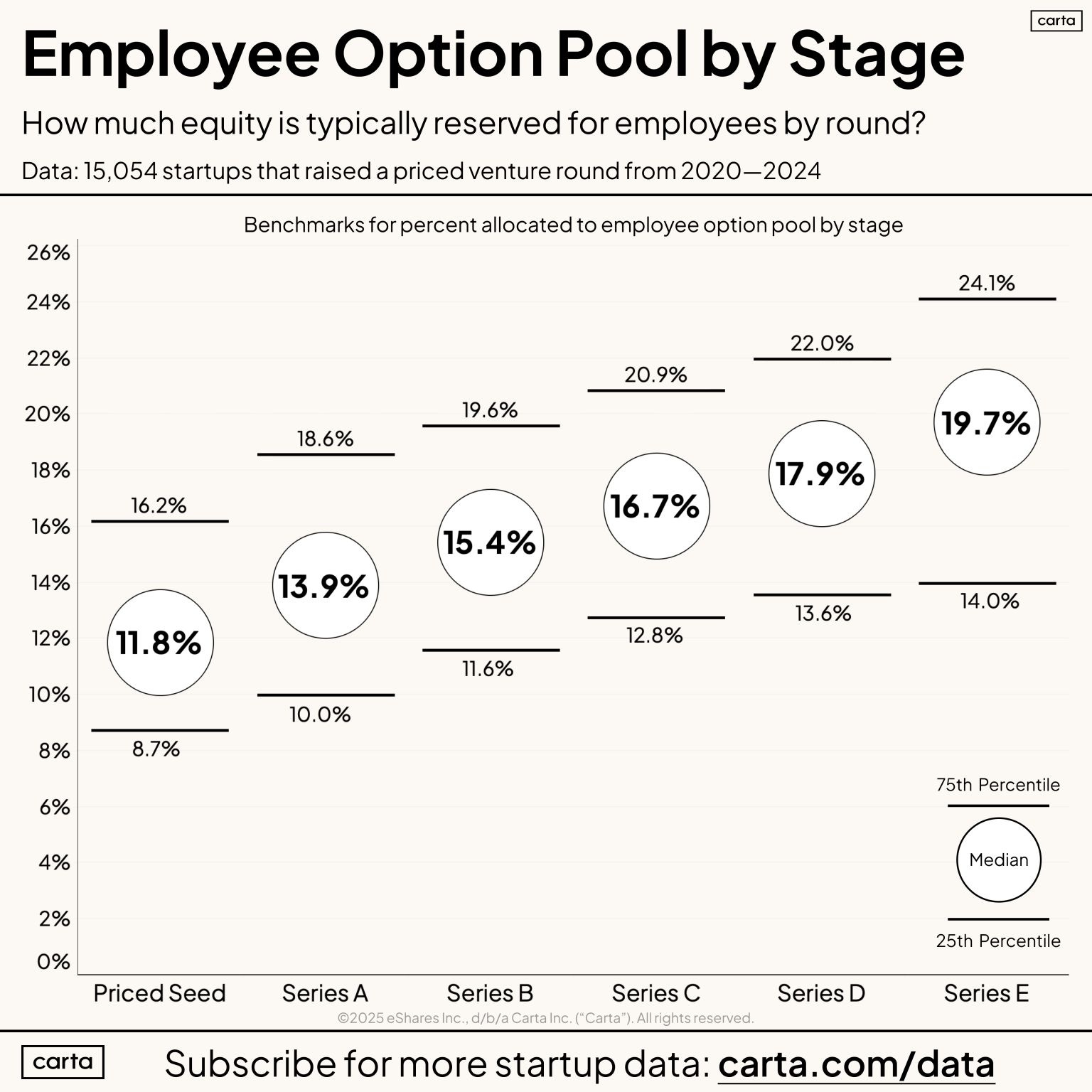

How Big Should Your Seed-Stage Employee Option Pool Be?

New data from Carta shows that the median employee option pool at the seed stage is significantly smaller than what some VCs may suggest. Here’s what you should know to balance employee fairness with founder equity preservation.

Option Pool Reality: Data from over 15,000 startups between 2020–2024 shows the median seed-stage employee pool is 11.8%, with the 75th percentile at 16.2%.

Why VCs Push Bigger Pools: Larger pools pre-round reduce their dilution but may over-allocate equity founders can later reclaim. On average, startups only use 60–70% of the pool before their next fundraising.

Planning for Growth: Seed-stage startups have slowed hiring compared to past years. Instead of overcommitting equity upfront, reserve enough for two years of hiring with the flexibility to replenish later.

✈️ KEY TAKEAWAYS

Founders should push back against unnecessarily large option pools in early rounds, leveraging data to preserve their equity while still supporting employee ownership.

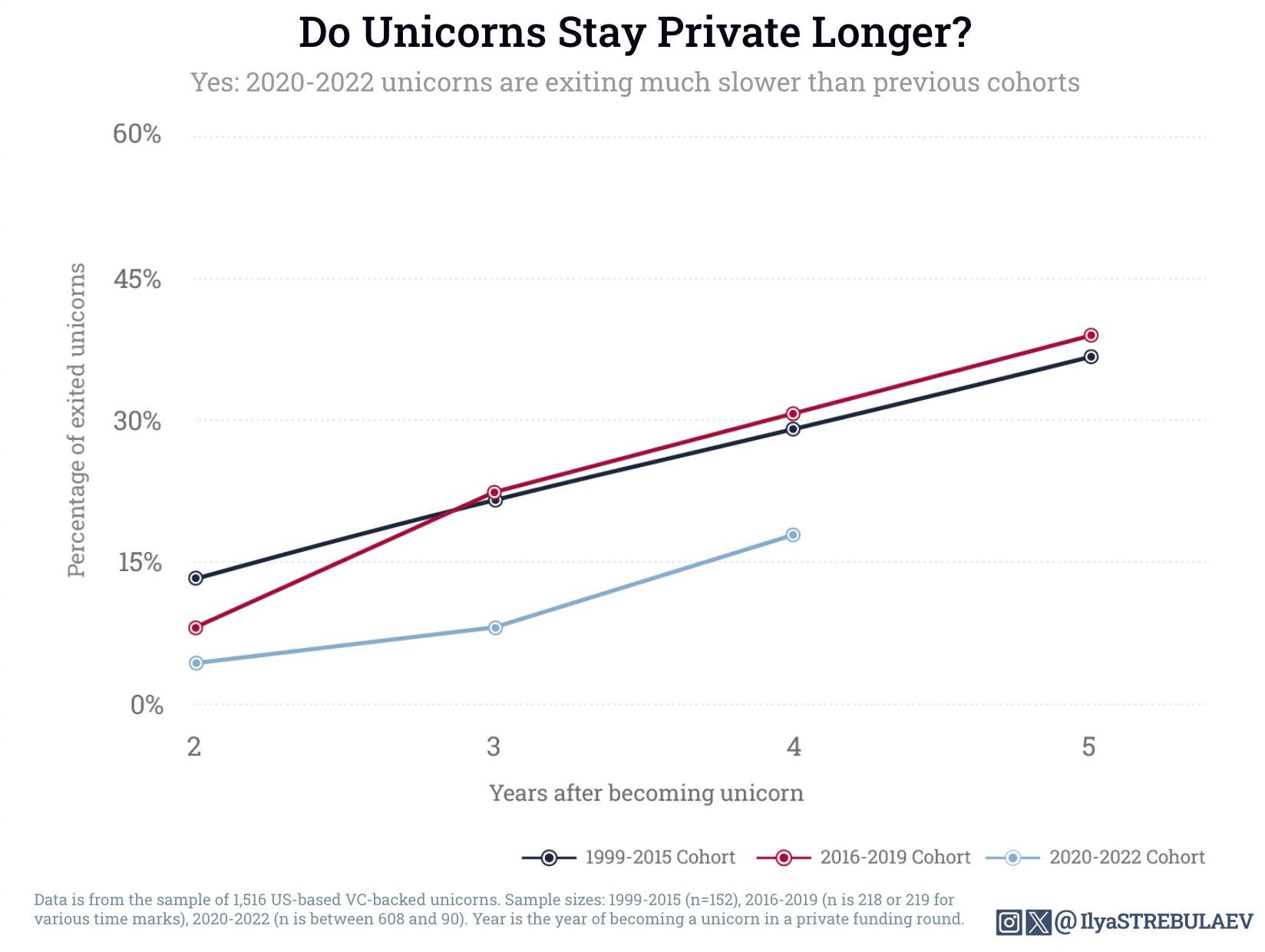

The Rise of Patient Unicorns: Longer Waits for Exits

Unicorn startups stay private longer, with recent cohorts showing historically low exit rates. A Stanford GSB study analyzed 1,516 US-based unicorns between 1997–2024, uncovering dramatic shifts in exit timelines.

Exit Rates in Early Years: The 1997–2015 cohort saw 18% of unicorns exit within 2 years, compared to just 6% in the 2020–2022 cohort.

Later Exit Trends: By year 5, roughly half of unicorns in earlier cohorts exited: 49% of the 1997–2015 cohort and 52% of the 2016–2019 cohort. The 2020–2022 cohort lags far behind, with only 11% exiting by year 3.

Patience Required: For all cohorts, a significant portion of unicorns remain private for at least 5 years, requiring investors to prepare for longer waits for returns.

✈️ KEY TAKEAWAYS

Recent unicorns are breaking the mold, with slower exit timelines and longer private growth phases, signaling a fundamental change in investor expectations.