👋 Hi, I’m Andre and welcome to my newsletter Data-Driven VC which is all about becoming a better investor with Data & AI. Join 33,310 thought leaders from VCs like a16z, Accel, Index, Sequoia, and more to understand how startup investing becomes more data-driven, why it matters, and what it means for you.

Brought to you by Affinity – Navigating 2025’s Investment Landscape

Market consolidation is reshaping venture capital, with fewer firms capturing the lion’s share of deals. How can investors adapt their dealmaking strategies to stay ahead?

Join Mercedes Bent, Venture Partner at Lightspeed, and Brian Murphy, Lead Data Scientist at Salesforce Ventures on May 8 for key insights on evolving dealmaking trends, the behaviors of top-performing firms, and the strategies investors are using to thrive in a competitive market.

Welcome to our monthly wrap-up episode where we cover April’s most relevant content at the intersection of startups, VC, data & AI.

We read it all so you don’t need to - here we go👇

INTERESTING RESEARCH & REPORTS📈

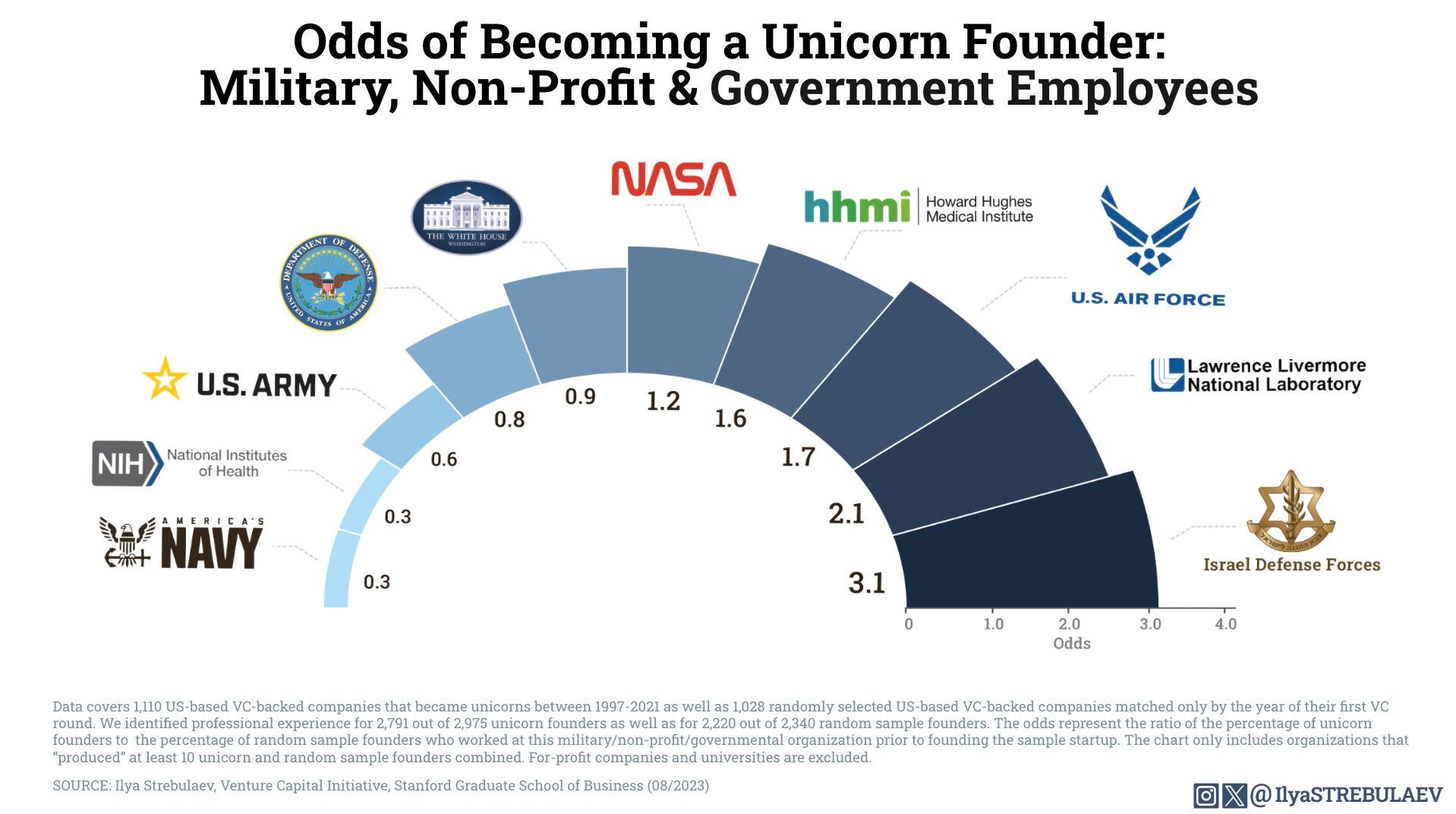

Where Unicorn Founders Come From

Stanford GSB’s Ilya Strebulaev analyzed 2,791 founders across 1,110 U.S.-based VC-backed unicorns to uncover the most common professional origins (and a few surprising ones) behind billion-dollar startups:

Academic & Military Hubs: Stanford and MIT dominate the educational backgrounds, while alumni of Israel’s IDF are 3x more likely to build unicorns than the average U.S. founder.

Prior Startup Experience: 40% of unicorn founders had previously launched a startup, giving them a repeat-founder advantage in venture growth.

Research Labs: 25% of unicorn founders came from scientific research or tech development roles, highlighting that deep R&D backgrounds can be just as valuable as startup hustle.

How military, non-profit, and governmental experience shapes the odds of becoming a unicorn founder (Strebulaev, 2025)

✈️ KEY TAKEAWAYS

Elite schools and military service aren’t the only pipelines to unicorn status—experience in research and tech development plays an underrated but significant role in startup success.

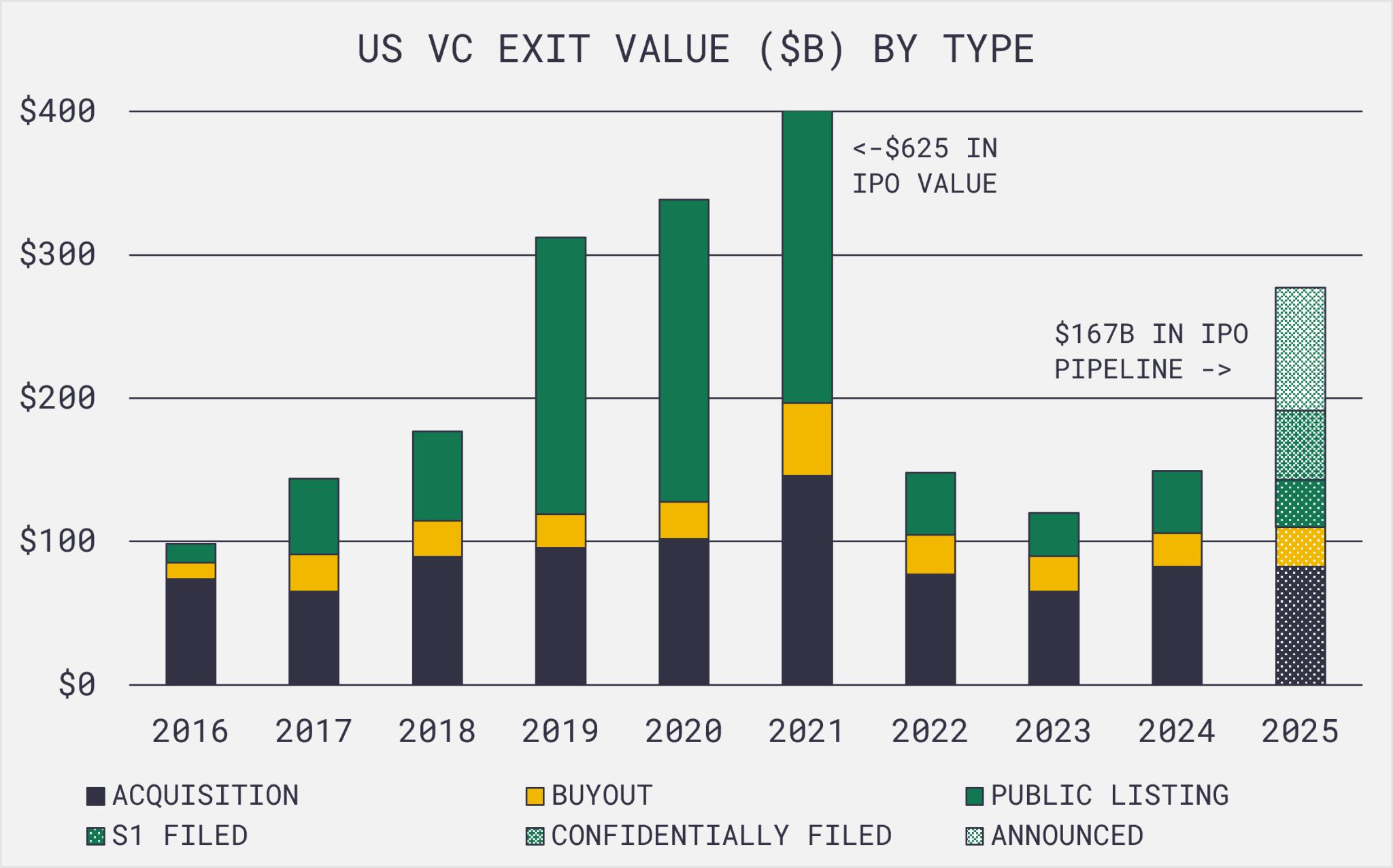

The 2025 Liquidity Puzzle

Jackie DiMonte’s latest analysis dives into whether 2025 could finally spark a liquidity wave amid years of muted exit values and locked capital. The article lays out a compelling data breakdown to question if we’re seeing the start of a sustained surge in liquidity or merely a small trickle.

Capital Lock-Up: Three years of depressed exit values echo early 2010s levels, even though a surge of capital flowed during 2020–2022, resulting in over 800 unicorns still waiting for an exit.

IPO Activity Surge: Data from the Forge Tech IPO Calendar shows over 30 companies have either filed or announced IPOs, representing up to $167B in last private market value, with S1 filings around $33B, confidential filings at $48B, and announced deals topping $86B.

Acquisitions & Exit Trends: Notably, Google’s recent $32B acquisition of Wiz underscores a broader trend where acquisitions are trending upward, making up 40% of last year’s total and hinting at a potential rebound in overall exit value.

Exit values summed up, from the linked article.

✈️ KEY TAKEAWAYS

The article suggests that despite years of tepid exit activity and significant capital still locked up, the surge in IPO filings and strategic acquisitions might signal the early stages of a liquidity wave, though the scale remains uncertain.